Summary of 2017 China Semiconductor Market Annual Meeting (essence Edition): 13 wonderful reports tell you the future of China's semiconductor industry

From March 23 to 24, the 2017 China Semiconductor Market Annual Conference was held in Nanjing. Many important guests from the Ministry of industry and information technology, big fund, Tsinghua University, SMIC international, Changdian technology, TSMC and other units attended and delivered wonderful speeches. We have sorted out the core points of 12 excellent reports for your reference.

Report summary:

Development status of global semiconductor industry. In 2016, the global semiconductor market reached US $338.93 billion, with a slight year-on-year increase of 1.1%. The regional market is polarized, with Europe and the United States showing a downward trend while Asia showing a growth trend. According to the statistics of China Semiconductor Industry Association, the sales volume of China's integrated circuit industry reached 433.55 billion yuan in 2016, with a year-on-year increase of 20.1%. The sales of design, manufacturing and seal testing industries were 164.43 billion, 112.69 billion and 156.43 billion respectively, with growth rates of 24.1%, 25.1% and 13% respectively. The growth rate of design and manufacturing was significantly faster than that of seal testing, with the proportion further rising, and the industrial structure tending to balance.

The development opportunities of China's integrated circuits are mainly reflected in: 1) huge market scale and strong market demand. In 2016, the scale of China's IC market was 119859 billion yuan, accounting for more than half of the global market. 2) A globalized market pattern and an active capital market. The world's top 20 integrated circuit enterprises have set up R & D centers, production bases and other branches in China. Chinese integrated circuit enterprises are actively integrating into the global integrated circuit industry. 3) The world's largest market and high market growth rate. It is expected that China will remain the world's largest integrated circuit market in the next few years and will maintain a high annual growth rate. The current challenges facing China's integrated circuit industry are: 1) the overall strength is insufficient: the domestic wafer manufacturing technology lags behind the world's leading level by two generations, the scale of the integrated circuit design industry accounts for less than 8% of the world, the integrated circuit industrial structure still needs to be optimized, and there is a lack of large-scale IDM enterprises; 2) Inefficient use of capital: Although the investment in fixed assets has increased, it has caused the problem of scattered investment. 3) The challenge of limited international integration has caused "excessive attention", and international M & A projects involving Chinese enterprises or capital have been rejected repeatedly.

The development of market and technology promotes the change of OSAT industrial model: 1) the rise of SIP. Mobile communication and IOT applications promote miniaturization and modularization, while SIP has the advantages of miniaturization, high integration and flexible design, which is very suitable for the technical requirements of these applications. 2) The rise of fo-wlp. Fo-wlp represents the innovation of the "third wave" packaging technology. It is expected that the CAGR will reach more than 30% in the next few years (2015-2020), far exceeding the single digit growth expectation of the overall market. 3) The rise of China. China has become a strategic market for semiconductor suppliers and OSAT.

The industry prosperity has entered an upward cycle, and the domestic semiconductor industry chain investment opportunities are sorted out in four dimensions. 1) From the perspective of application market, the investment opportunities of the semiconductor industry are mainly in emerging high growth fields such as mobile phone innovation, Internet of things, automotive electronics and intelligent hardware; 2) From the perspective of technological innovation, SIP / fanout advanced packaging, 3dic, compound semiconductor, new memory and other aspects deserve attention; 3) Focus on the trend of wafer manufacturing, packaging and test outsourcing from the perspective of industrial division of labor; 4) Focus on domestic production line construction and overseas M & A opportunities from the perspective of industrial transfer.

Report 1: China's integrated circuit industry with innovative and integrated development

Long Hanbing, electronic information department, Ministry of industry and information technology

Main points

1. Current situation of China's integrated circuit industry

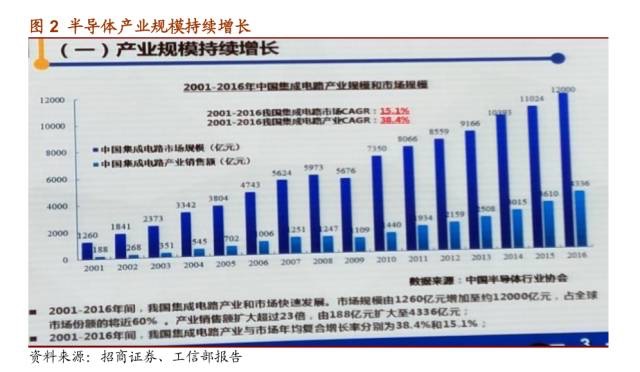

1) The industrial scale continued to grow. From 2001 to 2016, the scale of China's integrated circuit market increased from 126 billion yuan to about 120 billion yuan, accounting for nearly 60% of the global market share. The industrial sales volume expanded more than 23 times, from 18.8 billion yuan to 433.6 billion yuan. From 2001 to 2016, the compound growth rate of China's integrated circuit industry and market was 38.4% and 15.1% respectively.

2) The industrial structure tends to be rational. From 2001 to 2016, China's three integrated circuit industries (packaging, manufacturing and Design) went hand in hand, with an average annual compound growth rate of 36.9%, 28.2% and 16.4% respectively. Among them, the proportion of the design industry and the manufacturing industry is constantly increasing, and the industrial structure of integrated circuits tends to be optimized.

3) The development environment is constantly improving. Beijing, Sichuan, Shandong, Anhui, Tianjin and other provinces and cities have responded to the outline one after another and issued supporting policies to promote the industrial development of the region. At the same time, the national integrated circuit industry investment fund and local funds have been set up one after another, easing the bottleneck of investment and financing, and the prying effect is increasingly obvious.

Driven by market demand and supported by national policies, China's integrated circuit industry has initially possessed the foundation for participating in international market competition and supporting the development of information technology industry; The implementation of relevant national strategies has stimulated the internal vitality of the market, further optimized the development environment, and achieved steady and rapid development of the industry.

4) The core position is increasingly prominent. China's manufacturing industry is generally large but not strong. Most industries are still at the middle and low end of the value chain. In "made in China 2025", integrated circuits will be placed in the first place in the development of the new generation of information technology industry, which will drive the leap forward development of the integrated circuit industry.

2. New pattern and new challenges

1) Market driven transformation. The traditional PC business has further shrunk, and the market demand for intelligent terminals has gradually slowed down; And the demand for cloud computing, big data and industrial Internet has shown explosive growth. From 2011 to 2016, the global smartphone shipments continued to rise, while the global PC shipments showed a downward trend.

2) Transformation of innovation elements.

(1) Innovation based on single point and single product is changing to system innovation based on multi technology integration; (2) The development of cloud computing and big data will lead to changes in computing architecture, and new structures, new processes and new materials will bring about great changes; (3) Business model innovation becomes the key force of development; (4) The ability to integrate the elements of industrial development becomes the key to development; (5) Whether the ecological environment is perfect or not has become a new highland of international competition.

3) The change of competition pattern. In 2016, the global M & A in the integrated circuit field was active, with a transaction capital of more than 120 billion US dollars. Strong power combination and cross-border integration became a new trend.

4) Changes in the external environment. The major developed countries and regions in the world have further strengthened the government's attention to the development of the semiconductor industry.

5) The transformation of internal and external contradictions.

(1) The urgent requirement of leapfrog development of industry vs the lack of ability of backbone enterprises; (2) Complex and diversified market demand vs single product structure; (3) Rapid development of enterprises vs shortage of high-end talents; (4) Active international cooperation and M & A vs. countries increasing industrial supervision.

3. Future development direction

1) We will pay more attention to opening up and development. While adhering to independent innovation, we should strengthen international cooperation, make full use of global technology, talent, market, capital and other essential resources, and integrate into the global integrated circuit industry system. We will promote the healthy connection between industrial capital and financial capital, and promote international mergers and acquisitions.

2) Pay more attention to innovation and development. Deploy the innovation chain and the corresponding capital chain according to the industrial chain, and focus on cultivating enterprise innovation subjects; Strive to arrange the opportunity of disruptive technological change in advance; Implement made in China 2025, build an integrated circuit innovation center, and build a common key technology platform.

3) Pay more attention to focused development. Concentrate resources, backbone enterprises and key technology nodes to organize the implementation of national major special projects and industrial transformation and upgrading funds, and make breakthroughs in key core technologies and major products. We implemented the important deployment of strengthening supply side structural reform, and formulated plans to improve the effective supply capacity of key integrated circuit products and smart sensing action plans.

4) Pay more attention to coordinated development.

(1) Strengthen the organization and coordination of upstream and downstream resources of the industrial chain around major market demands; (2) Promote the establishment and improvement of industrial ecological environment; (3) Promote the layout and construction of major productive forces, strengthen the key links of the industry, and make up the weak links of the industry; (4) Strengthen the cooperation between industrial capital and financial capital to form a joint force for development; (5) Promote relevant documents, focus on solving problems in policy implementation, and further create a good policy environment.

5) Pay more attention to rational distribution and development. It mainly focuses on the layout of major productivity, such as vigorously improving the advanced process manufacturing capacity, accelerating the large-scale mass production of memory chips, vigorously developing the characteristic manufacturing process, improving the scale and level of the integrated circuit design industry, promoting the application and development of compound semiconductor devices, accelerating the upgrading and expansion of the sealing and testing industry, merger and reorganization, and enhancing the supporting capacity of key equipment and materials.

Report II: integration and innovation become the core driving force for the development of China's information industry

Ni Guangnan, academician of the Chinese Academy of Engineering

Main points

Integrated innovation is the core driving force for the development of China's information industry. It is conducive to the support of the new generation of information technology, promoting the in-depth and cross-border integration of various economic and social fields and industries, and further promoting economic globalization. Mainly reflected in the following aspects:

1. In terms of industrial Internet, China's advantages mainly lie in the universal application of the Internet, which is conducive to the realization of intelligent production control, intelligent operation decision optimization, and accurate connection between consumption demand and production and manufacturing.

2. In the field of military civilian integration, we will unswervingly follow the road of military civilian integration innovation and integrate the military innovation system into the national innovation system so as to achieve the compatible and synchronous development of the two.

3. In the field of network information, software and hardware, products and services have been deeply integrated, forming many new formats and modes, such as SDX and xaas.

4. The integration of disciplines is also essential. For example, artificial intelligence involves many disciplines such as computer, mathematics, psychology and linguistics, and there is a huge space for future development.

China has made some innovations in the field of wechat. For example, the Yuanxin mobile operating system OS developed in China has the characteristics of self-control and high security, and can be applied to smart phones, mobile office solutions, wearable embedded devices and Internet of things solutions.

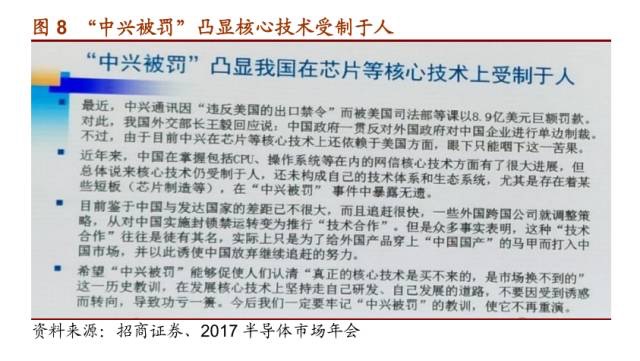

The core technology is controlled by others, which is the biggest hidden danger in China. The event of "SMIC being punished" highlights this point. Therefore, China should strengthen the research and development of core technologies, master core technologies as soon as possible, and make full use of the role of market-oriented guidance.

报告三、合作共赢,推动集成电路产业可持续发展

中国半导体行业协会副理事长 陈南翔

主要观点

2016年全球半导体市场规模小幅增长。2016年全球半导体市场规模达到3389.3亿美元,同比小幅增长1.1%。区域市场两极分化,欧美地区呈下滑态势(其中美国市场下降4.7%,欧洲市场下降4.5%),而亚洲地区呈增长态势(其中亚太增长3.6%,日本增长3.8%)。

中国集成电路产业保持快速增长。根据中国半导体行业协会统计,2016年中国集成电路产业销售额达到4335.5亿元,同比增长20.1%。设计、制造、封测三个产业销售额分别为1644.3亿、1126.9亿及1564.3亿,设计和制造环节增速明显快于封测,占比进一步上升,产业结构趋于平衡。

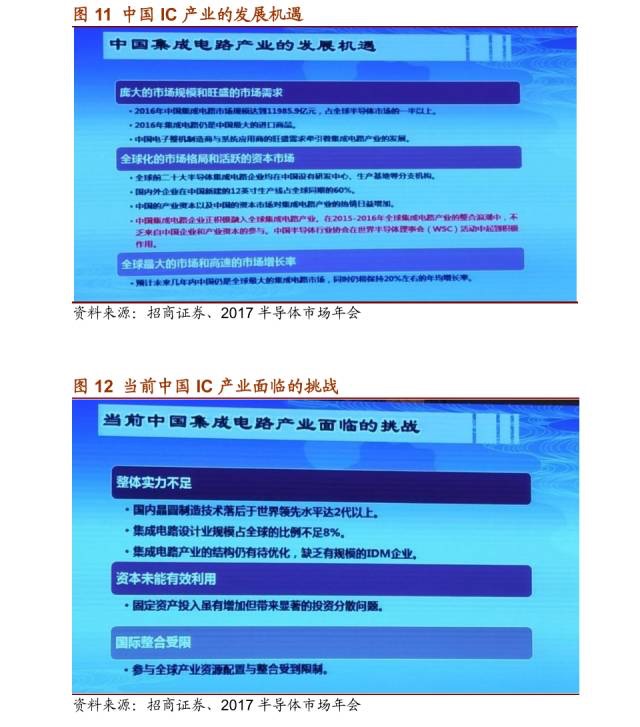

中国集成电路的发展机遇主要体现在:

庞大的市场规模和旺盛的市场需求。2016年中国集成电路的市场规模达到11985.9亿元,占全球半导体市场的一半以上。

全球化的市场格局和活跃的资本市场。全球前二十大半导体集成电路企业均在中国设有研发中心、生产基地等分支机构。另外,中国集成电路企业正在积极融入全球集成电路产业。

全球最大的市场和高速的市场增长率。预计未来几年内中国仍是全球最大的集成电路市场,且将保持20%左右的年均增长率。

中国目前面临整体实力不足、资本未有效利用以及国际整合受限的挑战。其中,中国还遭受“过度关注”,屡屡发生中国企业或资本参与的国际并购项目被否决。

2015-2016年全球近2000亿美元的产业整合中,中国企业和中国产业资本成功参与并购的项目金额不足全球的6%,但还是被贴上各种各样的“标签”,市场化和透明化运作的国家集成电路产业基金,规模与作用均被国际媒体严重扭曲。

报告四、硅世代4.0:人类智慧应用时代新核心

台湾半导体行业协会理事长 卢超群

主要观点

2016年全球半导体市场规模达3389亿美元,2017年市场规模3461亿美元。2016年台湾半导体产值达新台币2兆4493亿元,年成长率达8.2%,预估2017年可再成长5.8%。

半导体集成电路作为微电子器件的基础部件,正在例如实时视频流、无人机、机器人安全系统、可穿戴装置等新型科技产品的应用中扮演重要的核心地位。

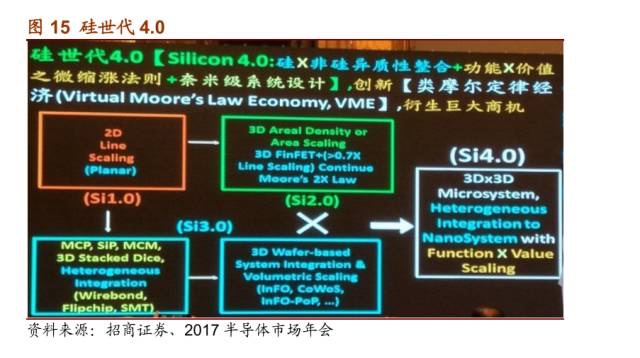

半导体集成电路行业的摩尔定律已经引领了50年的经济成长。

硅世代2.0的标志是以面积微缩法则为创新点的对于有效摩尔定律的促成,从而维持经济投资的效益。

硅世代3.0的标志是以体积微缩法则为创新点,对于有效摩尔定律经济的进一步促进作用。

异质性整合作为新型系统芯片整合技术大力推进了多维度集成芯片产业的发展。

基于晶圆注塑与无衬底的细距金属加工工艺,TSMC公司已能够将集成扇出封装技术实现量产化,从而有效地减小器件厚度、提升了工作性能、并降低成本,由此为移动计算产品的发展奠定基础。

硅世代4.0(硅X非硅异质性整合+功能X价值之微缩涨法则+纳米级系统设计),创新(类摩尔定律经济),衍生巨大商机。

报告五、中国集成电路供给侧结构分析

清华大学微纳电子学系主任 魏少军教授

主要观点

1、中国集成电路产业发展近况

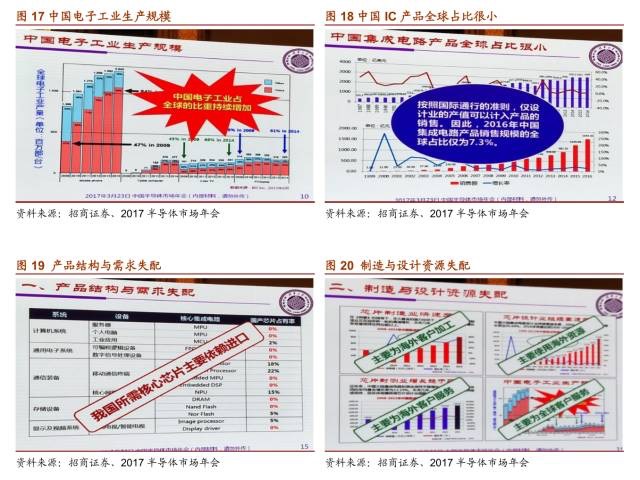

2016年中国集成电路产业销售额达到4435.5亿元,比上年增长20.1%,继续高速增长势头。

产业结构上,芯片设计业与芯片制造也所占比重呈上升趋势。芯片设计业增长24.1%,占全球IC设计比重的27.82%。

2、需求旺盛、供给不足将是长期矛盾

中国电子工业占全球的比重持续增加,中国大陆半导体市场规模为约835亿美元。2016年中国IC产品销售规模的全球占比仅为7.3%。

2016年中国集成电路进口额2270亿美元,持续维持高位。

3、中国集成电路供给侧结构分析

产品结构与需求失配:所需核心芯片主要依赖进口。制造与设计资源失配,制造业和设计业能力不足。投资略显凌乱,生产线建设缺少统筹。技术研发投入不足,人才团队严重短缺。

4、外部发展环境预判

半导体产业并购增多,西方对我国集成电路产业高度警觉。

产业发展的不确定性增加。

5、以非对称技术赢得发展主动权

6、总结

全球集成电路产业已经迈入成熟期,但集成电路技术还会继续演进,集成电路还将长期扮演核心关键角色,事实上,到现在为止还没有出现集成电路的替代技术。

中国已经成为全球最大的集成电路市场。产业布局基本合理,各领域进步明显。但集成电路的自给率不高,在很长一段时间内,对外依存度会维持在高位。

中国集成电路产业的结构性缺陷已经逐渐显现,“代工”模式一直主导着中国集成电路产业发展,但未来10-15年的发展是否还由这一模式主导值得探索。是时候研究中国集成电路供给侧的结构性变革这一课题了。

中国集成电路产业发展需要战略的判断力,实现路径的预见力,发展中国的战略定力,以及具体实施的执行力,创新能力才是根本。

报告六、IC封装的新趋势

江苏长电科技股份有限公司 高级副总裁 刘铭

主要观点

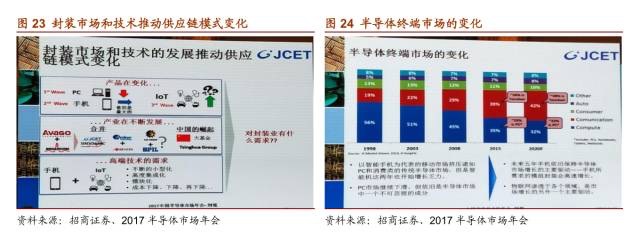

半导体终端市场发生变化。PC市场继续下滑,智能机开始增长乏力;未来手机所需求的模组封装会高速增长,物联网将渗透于各个领域。

物联网(loT)被认为是IC市场未来几年增长最快的领域。预计2019年IoT市场规模约为216亿美元,占全球半导体市场规模的6%,年均复合增长率为19%。

IoT模型涉及万物互联、通讯和网络、计算和存储、App和服务、大数据分析等五个层次,2020年市场规模均在百亿美元以上。

市场和技术的发展推动三个主要OSAT产业模式变化:

SiP的崛起。移动通讯和IoT应用会继续推动小型化和模块化,而系统级模块(SiP)具有小型化、高集成度、设计灵活等优势,非常适合这些应用的技术需求。

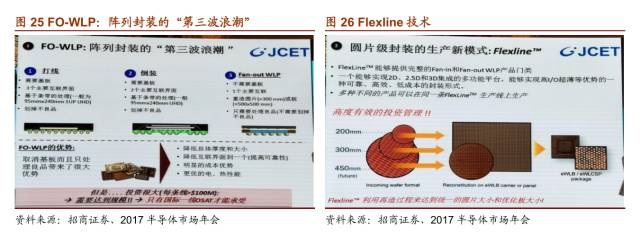

FO-WLP的崛起。FO-WLP代表了“第三波”封装技术的革新(打线—倒装—FO-WLP),预计在未来几年(2015-2020)年均复合增长率将达到30%以上,远超总体市场个位数的成长预期。

中国的崛起。中国成为半导体供应商和OSAT的战略市场,但由于技术原因本土设计公司采用本土OSAT并不多。在全球范围内,并购正在改变产业格局,2015年半导体公司并购协议的价值达102.4亿美元,中小型OSTA将越来越难满足主要客户对于产品广度和深度的需求。

告七、先进封测工艺发展的机遇与挑战

日月光集团副总裁 郭一凡

主要观点

先进封装技术的创新发展来自于摩尔定律的不断推进,未来封装技术的发展(挑战与创新)大都来自于新设计(应用)需求和新材料应用,并配合新工艺制程(设备)的研发实现。

未来半导体技术发展需要系统化设计,一体化解决方案要求封装必须与设计公司,材料/设备供应商密切合作开展研发,才能拓展和强化自身在产业链中的价值和创新作用,并和其它产业链中的环节一起共同创造半导体应用中的新技术。

报告八、加速创“芯”源自技术自信

北京华大九天软件有限公司 总经理 刘伟平

主要观点

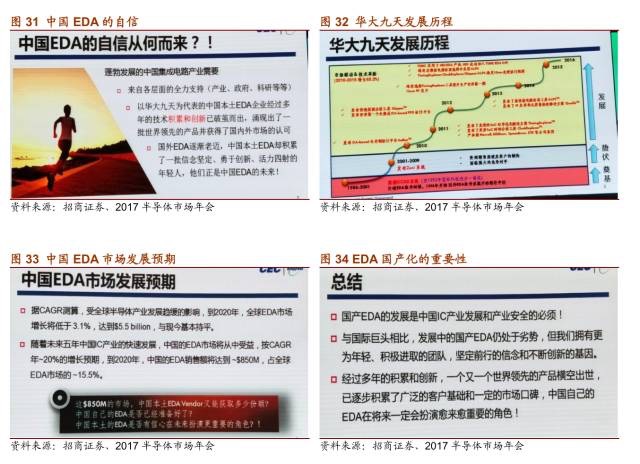

蓬勃发展的中国集成电产业离不开EDA的发展。

与国际巨头相比,国产EDA仍处于劣势,但国内进行全面的产品和技术积累,研发领先的SoC设计解决方案,具有广泛的国内外客户基础和密切的合作伙伴支持。

未来EDA市场发展预期。到2020年,全球EDA市场增长将低于3.1%,达到55亿美元,与现今基本持平。随着未来五年中国IC产业的快速发展,中国的EDA销售额将到达8.5亿美元,占全球EDA市场的15.5%。

报告九、化解供需矛盾,引导理性投资

赛迪顾问股份有限公司副总裁李珂

主要观点

1、中国集成电路市场发展呈现结构性矛盾

1)总体情况。2016年中国集成电路市场保持平稳增长,市场规模为11985.9亿元,未来3年CAGR达到7.8%。

2)从国内IC应用市场来看,汽车电子、工业控制领域将继续引领市场增长,2016年同比增速高达34.4%和21.0%。

3)在IC市场产品结构中,嵌入式产品与存储器市场需求旺盛,2016年同比增长率为18.8%,增速最快。

4)中国IC市场可以按照工艺线宽划分规模,其中28纳米以下工艺产品已占据国内集成电路市场半壁江山,2016年占比为53.4%。

5)供需总量上看,国内集成电路市场主要依赖进口局面。2016年中国集成电路产品进口额为2270.7亿美元,出口总额为613.8亿美元。

6)供需结构上看,国内仅有少量企业进入主流技术市场。28nm以下设计能力中海思、紫光展锐、中兴微排名前三,28nm以下制造能力中三星、中芯国际和海力士排名前三。

2、中国集成电路行业投资现状与对比

国内集成电路重点项目投资热情高涨。2016-2017Q1中国半导体行业重大项目投资公司包括紫光集团、台积电、格罗方德、联华电子等。

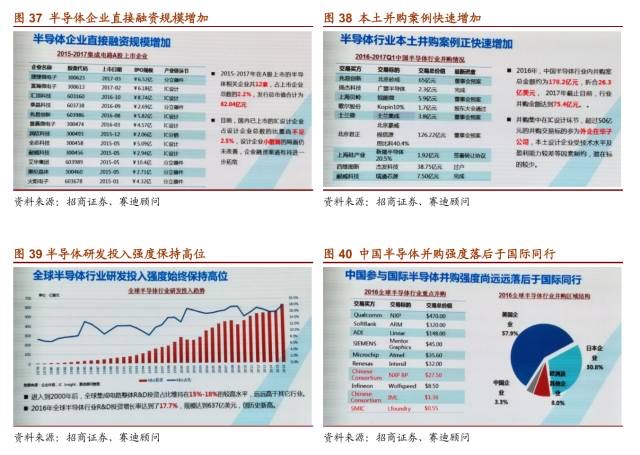

半导体企业直接融资规模增加。2015-2017年在A股上市的半导体相关企业共12家,占上市企业总数的2.2%,发行总市值合计为62.04亿元。然而,国内上市的IC设计企业占比较少,企业融资渠道有待进一步拓宽。

半导体行业本土并购案例正快速增加,但中国参与国际半导体并购强度远远落后于国际同行。2016年,中国半导体行业内并购案总金额为178.2亿元,2017年截止目前,行业并购金额达到75.4亿元。其中,并购集中在IC设计环节,由于本土设计企业受技术水平及盈利能力较差等因素的限制,超过50亿元的并购交易标的多为外企在华子公司。

国际半导体行业资本支出持续增长。近几年全球集成电路资本支出保持在600亿美元以上,其中投入金额最高的是IDM和FOUNDRY类企业。2016年,三星、TSMC、Intel的资本支出都在百亿美元左右。

全球半导体行业研发投入强度始终保持高位。进入2000年后,全球集成电路整体R&D投资占比维持在15%-18%的水平,远远高于其他行业。2016年全球半导体行业R&D投资增长率高达17.7%,规模达637亿美元,创历史新高。

国际主要半导体厂商R&D投入持续增长。2016年全球TOP10半导体企业R&D投资增长率达到17%,其中设计企业R&D投入占比较高,存储器芯片类企业占比相对较低。

3、未来发展建议

1)加大产业投资力度,提高市场供给能力;2)聚焦存储器、晶圆代工两大领域,集中力量重点突破;3)多种方式进行国际合作,理性开展行业并购。

报告十、洞烛先机,把握医疗电子新机遇

清华大学微电子学研究所副所长 王志华

主要观点

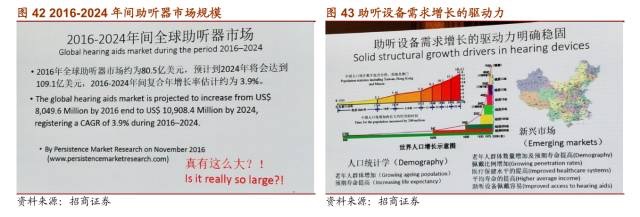

十年来医疗器械产业稳步发展,其中2016年强生、英特尔、美敦力的市场规模分别为25亿美元、59.387亿美元和28.833亿美元。2016-2024年间全球助听器市场。2016年全球助听器市场约为80.5亿美元,预计到2024年将会达到109.1亿美元,2016-2024年间复合年增长率估计约为3.9%。市场规模较大的原因主要有:

1)助听设备需求增长的驱动力明确稳固。随着医疗保健水平的提高,老年人群体数量增加且预期寿命提高,这对助听设备产生了巨大的需求。2)对于经合组织国家,助听器市场规模的增长潜在原因是上世纪的婴儿潮。3)中国正在加速进入老龄化时代。中国每年新增1000万,2030年将成为老龄化程度最高的国家,老年市场巨大且服务方式亟待创新。

助听器经历从听筒到数字技术的演变。助听器包含不同类型,例如无线互联的双耳助听以及智能双耳助听技术。

报告十一、二级市场半导体企业的机遇

招商证券研发中心电子行业首席分析师 鄢凡

主要观点

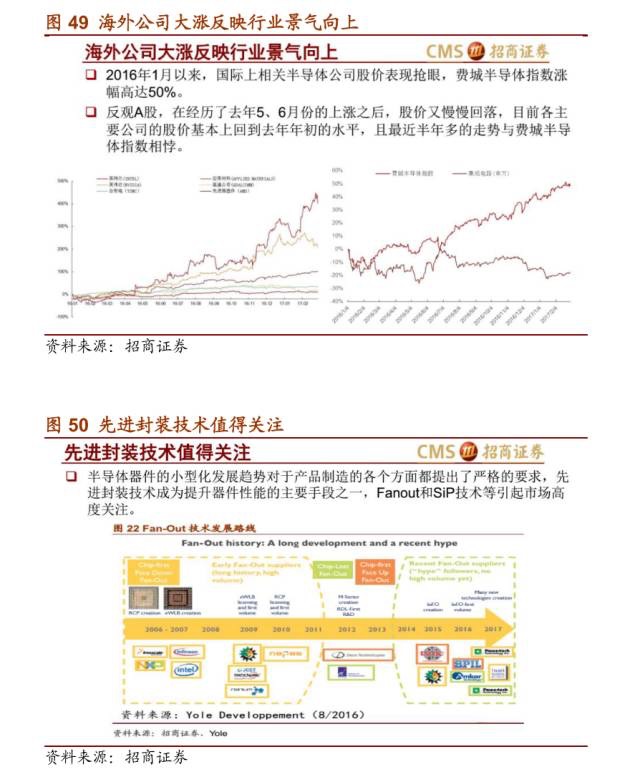

1、全球半导体产业面临新的形势

行业日趋成熟,行业规模增长速度放缓。主要原因是智能手机和计算机两大市场增长乏力,而新兴的物联网、汽车电子市场规模尚小,无法带动产业高增长。

半导体产业并购频发,巨头通过整合寻求新的增长方向。而中国资金的海外并购面临越来越大的挑战。

摩尔定律日益接近物理极限,延续摩尔定律面临挑战,先进封装等新技术引起市场广泛关注。

全球半导体行业分工模式继续发展,Fabless厂商的销售额增速明显高于IDM厂商。

当前半导体行业处于景气度向上周期。

2、中国半导体产业面临巨大发展机遇

进口替代、信息安全是国内发展半导体产业的核心逻辑。中国品牌的崛起拉动国内半导体需求增长。

中国政府大力扶持半导体产业发展,带动地方政府和社会资本的投资热情,加速半导体产业向大陆转移。大陆地区的半导体产业增长速度显著高于全球市场。

3、国内A股半导体产业投资值得关注的三个方向

国内生产线建设超预期;海外并购及其证券化;新市场和新技术带来的机会

报告十二、地方IC产业基金联动助力“弯道超车”

盛世投资合伙人 陈立志

2017年,在全面落实《国家集成电路产业发展推进纲要》的背景下,半导体产业也成为国家“十三五”规划的重中之重。随着国家促进集成电路产业的政策环境不断完善,以协同创新、开放合作为特征的国内集成电路产业正呈现出全新格局。在国家及各地各级政府的共同努力下,我国集成电路产业结构持续优化、集成电路市场稳定增长、企业创新能力进一步提升。

地方产业基金联动探索

千亿级国家集成电路产业投资基金撬动作用逐渐显现,各地相继设立专项扶持基金,产业融资瓶颈得到缓解,融资租赁等创新形式不断涌现。据陈立志介绍,为进一步落实《国家新兴战略产业发展规划》,培育集成电路产业全产业链条,加快推进集成电路产业整体升级,北京市于2014年设立北京集成电路产业发展股权投资基金,这是中国第一只集成电路产业母基金,盛世投资受托管理了该母基金。其所投制造子基金是国内第一只吸引国家集成电路产业投资基金参股的地方性产业基金,同时,该子基金引进了社会资本参与,形成了国家、市、区域、社会资本的有效协同。北京IC基金始终坚持多级联动探索,在央地联动、产融联动、各地联动等方面都做了有益实践。

集中力量推动集成电路产业“弯道超车”

今年,我国集成电路产业进入深度调整与转折期,这是我国实现“弯道超车”的机遇期,更是发展的攻坚期。陈立志表示,中国半导体产业与全球先进同行相比仍然存在很大的差距,作为政府引导基金,有别于市场化资本的一点,就是要勇于承担为国效力的重任,支持产业加大投入力度。

作为集成电路消费大国,我国集成电路市场仍严重依赖进口,“中国制造2025”、“互联网+”等国家战略的陆续实施将有力支撑产业实现跨越发展。对于产业跨国并购,陈立志认为,中国企业并非国际并购主力军,“两头在外”的现象没有根本改观,发达国家贸易保护主义抬头倾向明显。“凝聚力量、整合资源,修炼内功、自主创新”,才是实现产业跨越发展可行途径。

同时,作为国家信息安全和电子信息行业的基础,集成电路产业的被关注度不断提升,然而过度的宣传已经引起一些国家和地区不必要的警觉。陈立志呼吁,集成电路产业发展任重道远,还需要各界朋友的共同呵护,营造有利于产业发展的舆论环境

三个“坚持”促进集成电路产业健康有序发展

两年多来,在《国家集成电路产业发展推进纲要》的指引下,工信部与各省市持续推进集成电路产业协同发展,全行业保持了两位数的年均增长率,产业规模大幅提升,产业基金还将持续引领集成电路产业投资热潮。陈立志呼吁,一是坚持协同发力,国家大基金的设立,激活了各地集成电路产业的投资热情,实现了财政资金和社会资本共同投入,例如ISSI项目就是由北京、上海两地资本携手,壮大了中国资本[股评]的力量,使其得以被成功收购。二是坚持市场主导,《纲要》突出了以企业为主的市场导向,产业、资本都在挖掘优质项目,探索了区域内产融结合。三是坚持创新发展,各地着力解决产业“卡脖子”问题,仍需创新发展路径,建议在国家大基金牵头,各地政府、银行、投资机构联合推动一批重大、重点项目,促进产业有序、健康发展。

报告十三、融产结合,天高海阔

招商创投中心总经理 李鑫

集成电路领域是资本、人才、技术高度密集的一个领域。融产结合而非产融结合,因为现在中国存在一个大家显而易见的现象,是过去几十年存在的一个发展模式,很多实业的公司越来越不赚钱了,大家纷纷投入到很多虚拟金融行业,使的很多原来实业资本都跑到了金融圈里面,但是我们自己也清楚,实业如果不赚钱,那金融也只是无源之水。融产结合概念,是顺应国家现在所需要的这样一个转型课题,需要的是我们通过先进的资本组织的一些设立方式,科学的引导,把金融资本向产业资本来进行转移、转化,那背后的策略从国家还有我们行业内无非两个方面,一个是意义,一个是支持推动,一个意义就是现在国家大力来做,挤泡沫、去杠杆,推动的其实就是转型升级,还有我们的创新创业。

对于存量我们需要敞开自己的市场、自己的胸怀,充分进行国际转移、交流、合作。有关海外科技项目能够把他们引入到中国来落地,通过合资方式,而并不是收购。对于新的增量右手有两点。第一,通过和已有的全国各种双创平台进行合作,支持创新创业,设立了很多产业基金、种子基金。再有一点对于新的增量,对中国现在最重要其实是产业生态的共建,为了未来五年、十年中国在这个产业能够在全球真正迈向一个好的发展阶段需要打下一个基础。

以往结合海外并购和中国自己产业发展诉求,在不同阶段深化过程当中,海沟并购要素也不太一样,简单分为三个阶段。第一个阶段最初级,把一些产品线,一些财务报表利润收入进行合并融合,更高阶段希望融合相关细分领域重要的技术专利,进行我们短板不足。但是这点往往也是有缺陷的,因为专利技术都是以往国外研究取得成果,不代表未来这些领域仍然是这个样子。真正核心东西恰恰是人才,而且我们中国目前是全球最大的市场,最大的消费所在国,中国有强大的厂商,他们在产品设计、定义方面其实是有先天定义的优势,因此在下一个阶段,很多目前着手的海外订购,他们在关注已经上升到如何吸收海外的人才、平台,与中国有基础的项目进行很好的融合、提升,这如果实现的很好的话,会使未来出现国内未来有很多非常发展不错的长跑选手。

Service hotline Service time | Contact Us

|

Follow us |

ADD:Room 1006, Building A, Phoenix Zhigu, Country Garden, xixiang street, Baoan District, Shenzhen

ADD:Room 1006, Building A, Phoenix Zhigu, Country Garden, xixiang street, Baoan District, Shenzhen TEL:0755-83568817 0755-83568867

TEL:0755-83568817 0755-83568867 FAX:0755-83568658

FAX:0755-83568658